- Strategic Management - Manufacturing Performance

- 2026-05-19

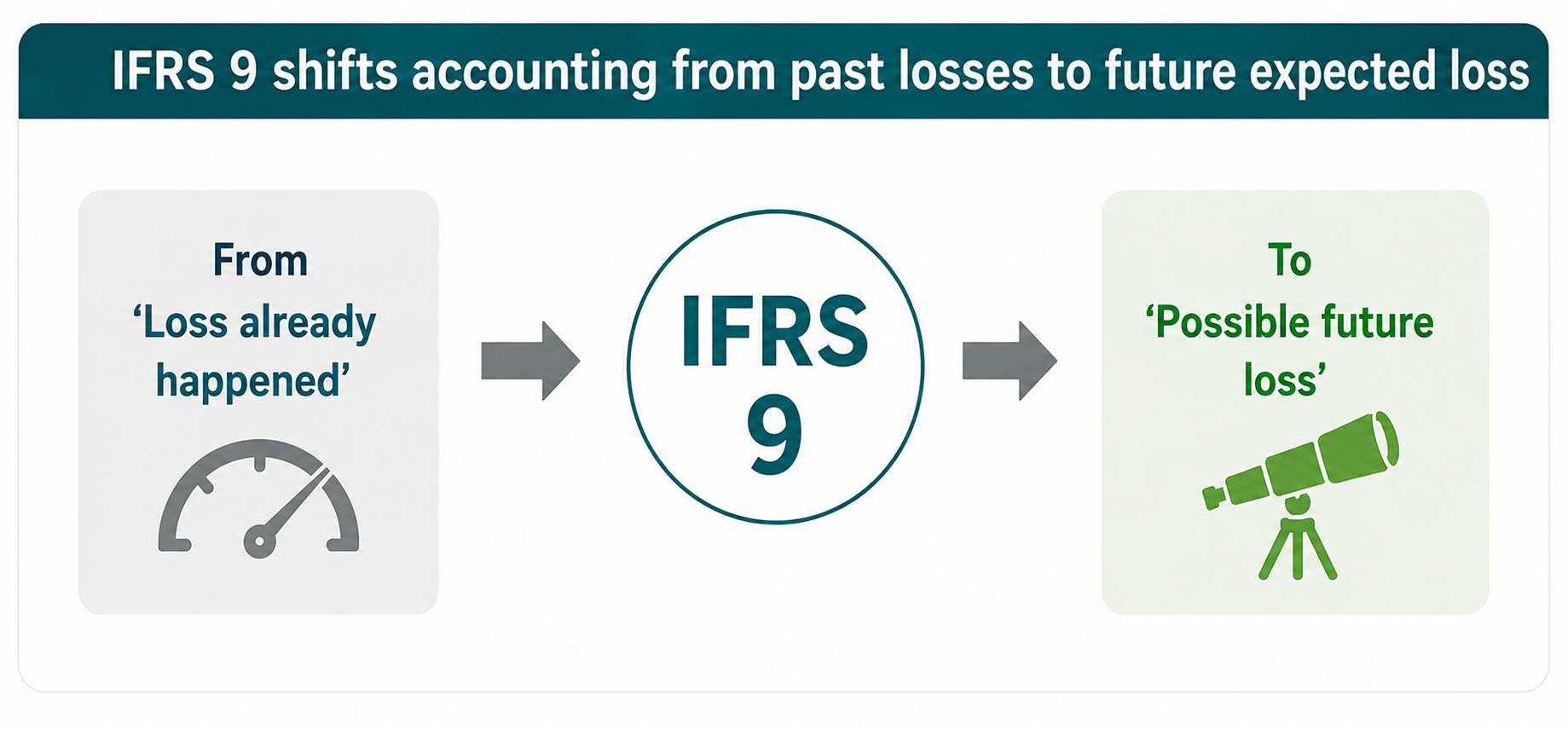

IFRS 9 — A Strategic Framework For Managing Financial Risk And Sustaining Long-Term Institutional Stability

One of the most significant transformations introduced by IFRS 9 is the replacement of the traditional incurred loss model with a forward-looking Expe...

Read More