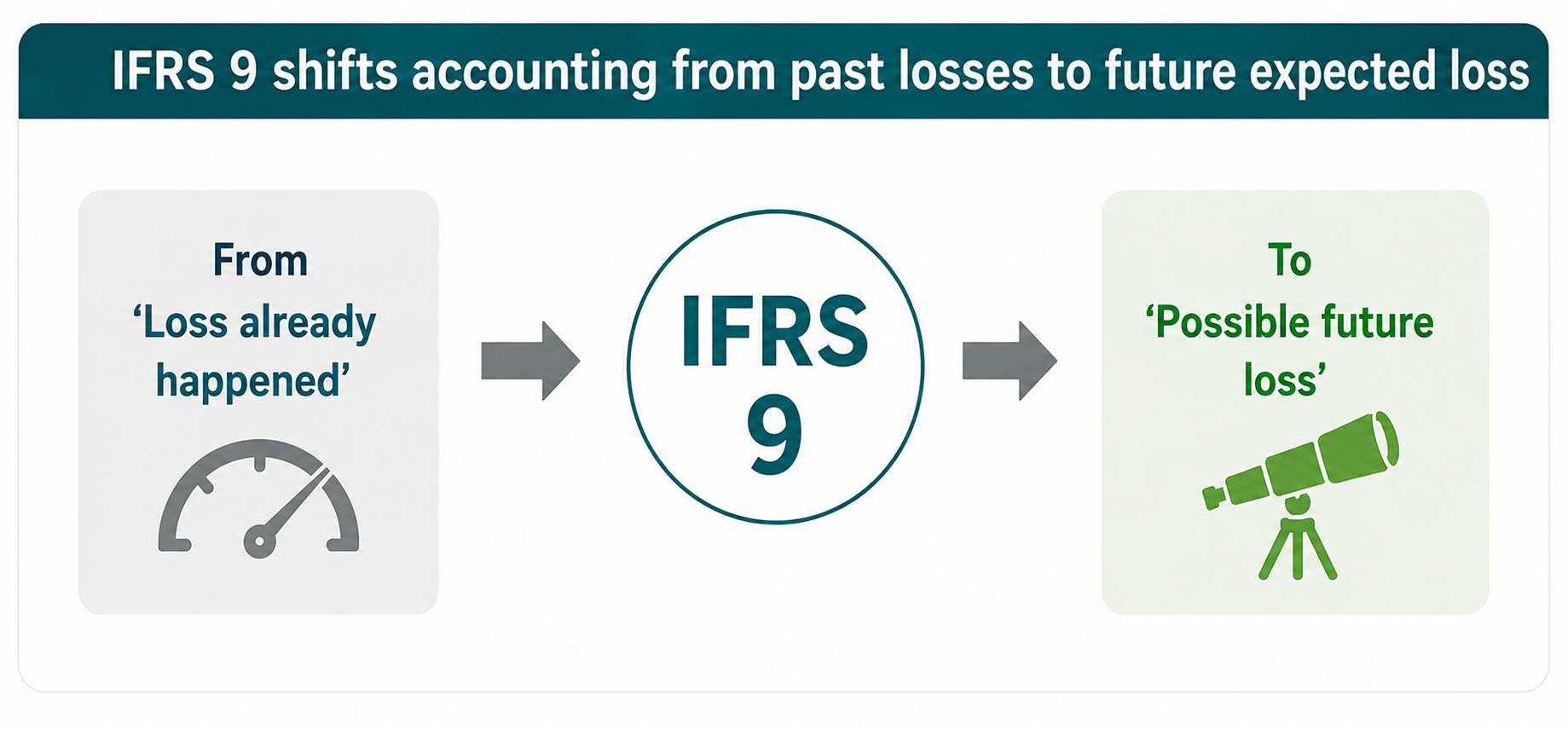

One of the most significant transformations introduced by IFRS 9 is the replacement of the traditional incurred loss model with a forward-looking Expected Credit Loss (ECL) model. Under previous practices, impairment losses were recognized only after objective evidence of loss had occurred. IFRS 9 fundamentally changed this approach by requiring entities—particularly banks and financial institutions—to recognize expected future credit losses at an earlier stage, even before actual default occurs. This shift enables proactive risk identification and enhances the reliability of financial reporting.

One of the most significant

transformations introduced by IFRS 9 is the replacement of the traditional incurred

loss model with a forward-looking Expected Credit Loss (ECL) model.

Under previous practices, impairment losses were recognized only after

objective evidence of loss had occurred. IFRS 9 fundamentally changed this

approach by requiring entities—particularly banks and financial institutions—to

recognize expected future credit losses at an earlier stage, even before

actual default occurs. This shift enables proactive risk identification and

enhances the reliability of financial reporting.

IFRS 9 is built around three principal areas:

1.

Classification and Measurement of

Financial Assets

Financial assets are classified based on:

- Business

Model Test: How an entity manages financial assets (hold to collect,

hold to collect and sell, or trading).

- SPPI

Test (Solely Payments of Principal and Interest): Whether contractual

cash flows represent only repayment of principal and interest.

Based on these assessments, financial assets are measured

under one of the following categories:

- Amortized

Cost

- Fair

Value Through Other Comprehensive Income (FVOCI)

- Fair

Value Through Profit or Loss (FVTPL)

The classification directly influences profit recognition,

valuation methods, and risk exposure.

2. Impairment through Expected Credit Loss (ECL)

The ECL model requires estimation of future credit losses

using both historical data and forward-looking economic information. Expected

losses are generally determined considering:

- Probability

of Default (PD)

- Loss

Given Default (LGD)

- Exposure

at Default (EAD)

- Macroeconomic

assumptions

- Industry

and borrower-specific risks

The ECL model operates under a three-stage impairment

framework:

|

Stage |

Credit

Condition |

Provision

Requirement |

|

Stage 1 |

Performing

asset |

12-month ECL |

|

Stage 2 |

Significant

increase in credit risk |

Lifetime ECL |

|

Stage 3 |

Credit-impaired/defaulted

asset |

Lifetime ECL

with net interest recognition |

This staging approach allows institutions to identify

deterioration in credit quality and increase provisions progressively.

3. Hedge Accounting

IFRS 9 aligns accounting treatment with actual risk

management strategies, improving the reflection of hedging activities in

financial statements and reducing inconsistencies between accounting and

economic outcomes.

Strategic Impact on Banking Sector

The implementation of IFRS 9 has substantially changed the

banking industry by integrating accounting with credit risk management. Major

impacts include:

- Higher

and earlier provisioning requirements

- Reduction

in profitability during economic stress

- Increased

volatility in earnings

- Greater

demand for data analytics and risk modeling

- Need

for advanced ERP, MIS, and Business Intelligence systems

- Enhanced

governance and regulatory oversight

- Influence

on capital adequacy and lending strategy

Banks are now required to maintain sophisticated credit risk

models, continuously monitor borrower behavior, and incorporate future economic

forecasts into impairment calculations.

IFRS 9 represents a paradigm

shift from reactive accounting toward forward-looking risk management.

By introducing Expected Credit Loss methodology, the standard encourages

earlier recognition of risk, enhances transparency, and strengthens financial

stability. Although implementation requires significant investment in systems,

data infrastructure, and expertise, IFRS 9 ultimately promotes more resilient

institutions, improved decision-making, and stronger governance across the

financial sector.

In essence, IFRS 9 is no longer merely an accounting

requirement—it has become a strategic framework for managing financial risk and

sustaining long-term institutional stability.